Let’s be honest. At its core, notes payable is just a company’s written promise to pay back money it has already spent. Think of it as a corporate IOU, but with more lawyers and a formal entry on your company’s balance sheet as a liability.

This liability pops up when your company issues a written promise, a.k.a. a promissory note, to a lender in exchange for cash. It’s your solemn vow to repay the money, plus a little extra something called interest.

So, What is Notes Payable in Accounting?

Notes payable represents the exact amount of money your business owes under the terms of that promissory note. You get a chunk of cash from a lender – usually a bank – and in return, you hand them a formal document promising to repay the principal amount, plus interest, by a specific date.

From the lender’s side of the table, this same promise is an asset, which they record as notes receivable. One person’s debt is another’s treasure, right?

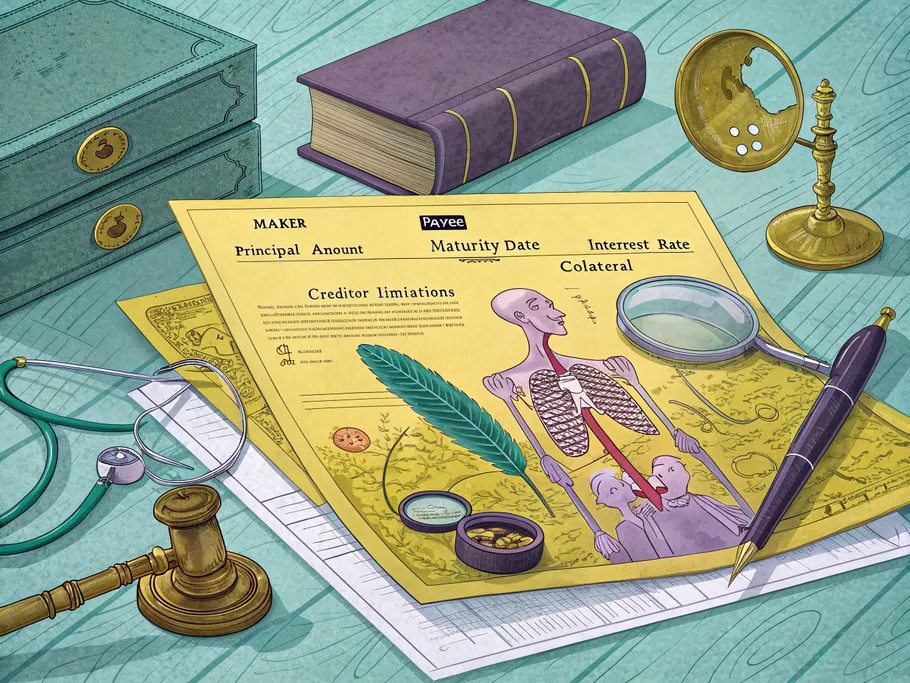

The Anatomy of a Promissory Note

A promissory note isn’t just a scribble on a napkin. It’s a formal document with some key players and terms:

- Maker: That’s you. The company issuing the note and on the hook for paying it back.

- Payee: The lender, the one who gets to cash in on your promise.

- Principal Amount: The initial pile of cash you borrowed.

- Maturity Date: The doomsday clock. The date when the principal and all accrued interest are due.

- Interest Rate: The price of borrowing money, shown as a percentage.

- Collateral: Assets you pledge as a security blanket for the lender in case you default.

- Creditor Limitations: And here’s the fun part. These are restrictions the lender imposes on you. Signing a promissory note? Congrats, you may have just given your lender the right to micromanage your business until payday, limiting things like dividend payments or stock buybacks.

Is Notes Payable a Liability or an Asset? The Existential Question

To get the notes payable classification right, you have to know the difference between what you have and what you owe.

- Assets are the fleeting illusions of wealth you might briefly possess. They are resources like cash, inventory, and equipment that are supposed to make you more money.

- Liabilities are the concrete, soul-crushing obligations proving you owe someone else. They are debts settled by giving away your precious money, goods, or services.

So, is notes payable a liability? Absolutely. It’s a signed promise to delay your financial obligations, with interest. The notes payable on balance sheet is always, without exception, listed in the liabilities section, staring back at you like a receipt for your ambition.

Is Notes Payable a Debit or Credit?

In the beautiful, balanced world of double-entry accounting, everything follows one simple equation:

Assets = Liabilities + Equity

Here’s how the rules shake out:

- Assets: Go up with a debit, down with a credit.

- Liabilities and Equity: Go up with a credit, down with a debit.

Since notes payable is a liability, its balance increases with a credit. When you first take out the loan, you credit the Notes Payable account.

- Increase in Notes Payable: You credit the account when you borrow money.

- Decrease in Notes Payable: You debit the account when you pay the money back.

Therefore, the normal balance for Notes Payable is always a credit.

How to Make a Notes Payable Journal Entry

Proper accounting for notes payable requires recording every step of the journey. Here’s the typical lifecycle of a note, broken down into journal entries.

Issuance of the Note

When you receive the cash, your assets (Cash) go up, and your liabilities (Notes Payable) go up.

- Debit: Cash (for the amount received)

- Credit: Notes Payable (for the same amount)

Interest Accrual

Time passes, and interest builds up. You have to record this expense as it’s incurred, even if you haven’t paid it yet. This is the magic of interest accrual.

- Debit: Interest Expense

- Credit: Interest Payable (a separate liability account for interest you owe)

Payment of Interest

When you make an interest payment, you reduce the liability you recorded and reduce your cash.

- Debit: Interest Payable

- Credit: Cash

Repayment of the Note Principal

On the maturity date, when you finally pay back the loan, you wipe the liability off your books.

- Debit: Notes Payable (for the principal amount)

- Credit: Cash

Notes Payable Examples in Action

Let’s see how this plays out in the real world.

Example 1: Construction Company Equipment Purchase

ABC Construction Company purchased a truck for $100,000 on credit from XYZ Motors. Unable to make prompt payment, ABC issued a promissory note with the following terms:

- Payee: XYZ Motors

- Maker: ABC Construction Company

- Principal: $100,000

- Maturity Date: 6 months

- Interest Rate: 6% per year

Journal Entry for Issuance: ABC records the liability.

- Debit Equipment $100,000

- Credit Notes Payable $100,000

Journal Entry for Interest Accrual at Maturity: The total interest for 6 months is ($100,000 × 6% × 6/12) = $3,000.

- Debit Interest Expense $3,000

- Credit Interest Payable $3,000

Journal Entry for Repayment at Maturity: ABC pays the principal and interest.

- Debit Notes Payable $100,000

- Debit Interest Payable $3,000

- Credit Cash $103,000

Example 2: Tractor Loan with Quarterly Interest

A company purchases a tractor with a $1,000,000 loan, formalized with a note payable. Interest is 5% per year, paid quarterly.

Journal Entry for Issuance:

- Debit Cash $1,000,000

- Credit Notes Payable $1,000,000

Journal Entry for Quarterly Interest Accrual: Quarterly interest is ($1,000,000 × 5% / 4) = $12,500.

- Debit Interest Expense $12,500

- Credit Interest Payable $12,500

Journal Entry for Quarterly Interest Payment:

- Debit Interest Payable $12,500

- Credit Cash $12,500

Journal Entry for Loan Repayment at Maturity:

- Debit Notes Payable $1,000,000

- Credit Cash $1,000,000

Example 3: Supplier Debt Conversion

Anne’s Online Store owes Cindy’s Apparel $15,000 for inventory. They agree to convert this debt into a formal note. The promissory note has a 10% annual interest rate and is due in 3 months.

Journal Entry for Conversion: Anne’s Online Store converts an account payable to a note payable.

- Debit Accounts Payable $15,000

- Credit Notes Payable $15,000

Journal Entry for Interest Accrual: At the end of 3 months, interest is ($15,000 × 10% × 3/12) = $375.

- Debit Interest Expense $375

- Credit Interest Payable $375

Journal Entry for Repayment:

- Debit Notes Payable $15,000

- Debit Interest Payable $375

- Credit Cash $15,375

Accounts Payable vs Notes Payable

While both are liabilities, they aren’t twins. The accounts payable vs notes payable distinction is crucial. Notes payable are formal, written agreements with specific repayment terms and interest, often used for big-ticket financing.

Accounts payable, on the other hand, are the informal IOUs you have with your suppliers for goods or services. They’re typically settled in 30 to 60 days and usually don’t have interest tacked on. Misclassifying these can distort your company’s financial health, so knowing the difference is key to smart cash flow management.

Here’s a simple breakdown:

| Feature | Notes Payable | Accounts Payable (A/P) |

|---|---|---|

| Formal Agreement | Based on a formal, written promissory note. | Represents informal amounts owed to suppliers. |

| Interest | Typically includes an explicit interest rate. | Usually does not involve interest payments. |

| Maturity Date | Has a specific, predetermined repayment date. | Due dates are short-term (e.g., 30-60 days). |